Această postare este a treia parte a https://thierrymoudiki.github.io/blog/2025/12/07/r/forecasting/ARIMA-Pricing și https://thierrymoudiki.github.io/blog/2026/02/01/r/Semi-parametric-MarketPriceofRisk-The. Aceste postări au arătat cum să utilizați ARIMA și Theta ca preț de piață al riscului, pentru a stabili apoi opțiunile în conformitate cu o măsură neutră din punct de vedere al riscului prin reeșantionare martingale inovații.

După ce m-am gândit mai mult la asta, iată o versiune condensată a postărilor anterioare, cu câteva formule și exemple bogate de cod R.

1. Stabilirea pieței

Lasă

- (S_t) = prețul activului

- (r) = rata fără risc

- (T) = maturitate

Definiți proces de preț redus

(D_t = e^{-rt} S_t)

Conform principiului fără arbitraj (teorema fundamentală a prețului activelor), există o măsură de probabilitate (Q) astfel încât

(E_Q(D_t mid mathcal{F}_{t-1}) = D_{t-1})

deci (D_t) este a martingale.

Având în vedere căile de preț simulate sau observate (S_t), calculați

(D_t = e^{-rt} S_t)

Definiți incremente

(Delta D_t = D_t – D_{t-1})

Montați un filtru de serie de timp

(Delta D_t = f(Delta D_{t-1}, ldots, Delta D_{tp}) + varepsilon_t)

unde

(E(varepsilon_t) = 0)

3. Distribuția inovației Bootstrap

Lasă

({varepsilon_1, ldots, varepsilon_T})

fie inovaţiile empirice.

Generați reeșantioane bootstrap

(varepsilon_t^{(i)}, quad i = 1, ldots, N)

folosind bootstrap staționar. Aceste secvențe definesc legea inovării.

4. Reconstrucție Martingale

Definiți recursiv procesul actualizat:

(D_0 = S_0) (D_t = D_{t-1} + varepsilon_t)

ceea ce presupune

(D_t = S_0 + sum_{i=1}^{t} varepsilon_i)

Din moment ce

(E(varepsilon_t) = 0)

obținem

(E(D_t) = E(S_0 + sum_{i=1}^{t} varepsilon_i) = S_0 + sum_{i=1}^{t} E(varepsilon_i) = S_0)

5. Proces de preț neutru față de risc

Recuperați procesul de preț

(S_t = e^{rt} D_t)

Apoi

(E(e^{-rt} S_t) = S_0)

care satisface stare de risc neutru.

6. Prețuri Monte Carlo

Pentru payoff (H(S_T)), prețul derivatului este

(V_0 = e^{-rT} E_Q(H(S_T)))

Estimată de Monte Carlo:

(V_0 aprox e^{-rT} frac{1}{N} sum_{i=1}^{N} H(S_T^{(i)}))

Exemplu (apel european):

(C_0 = e^{-rT} E_Q(max(S_T – K, 0)))

Iată codul R pentru întregul proces:

library(esgtoolkit)

library(forecast)

set.seed(123)

n <- 250L

h <- 5

freq <- "daily"

r <- 0.05

maturity <- 5

S0 <- 100

mu <- 0.08

sigma <- 0.04

n_sims <- 5000L

# Simulate under physical measure with stochastic volatility and jumps

sim_GBM <- esgtoolkit::simdiff(

n = n,

horizon = h,

frequency = freq,

x0 = S0,

theta1 = mu,

theta2 = sigma

)

sim_SVJD <- esgtoolkit::rsvjd(n = n, r0 = mu)

sim_Heston <- esgtoolkit::rsvjd(

n = n,

r0 = mu,

lambda = 0,

mu_J = 0,

sigma_J = 0

)

# This exp(-r*t)*S_t

discounted_prices_GBM <- esgtoolkit::esgdiscountfactor(r = r, X = sim_GBM)

discounted_prices_SVJD <- esgtoolkit::esgdiscountfactor(r = r, X = sim_SVJD)

discounted_prices_Heston <- esgtoolkit::esgdiscountfactor(r = r, X = sim_Heston)

# Take the first difference of exp(-r*t)*S_t

# (we want a center first difference in Q)

diff_martingale_GBM <- diff(discounted_prices_GBM)

diff_martingale_Heston <- diff(discounted_prices_Heston)

diff_martingale_SVJD <- diff(discounted_prices_SVJD)

# Adjust a time series filter the martingale difference

choice_process <- "GBM"

choice_filter <- "auto.arima"

diff_martingale <- switch(choice_process,

GBM = diff_martingale_GBM,

Heston = diff_martingale_Heston,

SVJD = diff_martingale_SVJD)

n_dates <- nrow(diff_martingale)

n_dates_1 <- n_dates - 1

resids_matrix <- matrix(0, nrow = n_dates_1, ncol = n)

pb <- utils::txtProgressBar(min = 0, max = n, style = 3L)

if (choice_filter == "AR(1)")

{

for (j in 1:n)

{

y <- diff_martingale(-1, j)

X <- matrix(diff_martingale(seq_len(n_dates_1), j), ncol = 1)

fit_lm <- .lm.fit(x = X, y = y)

fitted_values <- X %*% fit_lm$coef

resids_matrix(, j) <- y - fitted_values

utils::setTxtProgressBar(pb, j)

}

close(pb)

}

if (choice_filter == "auto.arima"){

for (j in 1:n)

{

y <- diff_martingale(-1, j)

resids_matrix(, j) <- residuals(auto.arima(y, allowmean = FALSE))

utils::setTxtProgressBar(pb, j)

}

close(pb)

}

pvals <- sapply(1:n, function(j)

Box.test(resids_matrix(, j), type = "Ljung-Box")$p.value)

# Keep only stationary residuals (non-reject null at 5% level)

stationary_cols <- which(pvals > 0.05)

resids_stationary <- resids_matrix(, stationary_cols)

print(dim(resids_stationary))

centered_resids_stationary <- scale(resids_stationary, center = TRUE, scale = FALSE)(, )

centered_resids_stationary <- ts(centered_resids_stationary,

end = end(sim_GBM),

frequency = frequency(sim_GBM))

# resample_centered_resids has nrow = number of dates, ncol = n_sims

resampled_centered_resids <- list()

n_resids_stationary <- dim(resids_stationary)(2)

n_times <- ceiling(n_sims/n_resids_stationary)

pb <- utils::txtProgressBar(min = 0, max = n_times, style = 3L)

for (i in seq_len(n_times))

{

set.seed(123 + i*100)

resampled_centered_resids((i)) <- apply(centered_resids_stationary, 2,

function(x) tseries::tsbootstrap(x, nb=1,

type="stationary"))

utils::setTxtProgressBar(pb, i)

}

close(pb)

resampled_centered_resids_matrix <- do.call(cbind, resampled_centered_resids)(, seq_len(n_sims))

# Convert to ts object with proper time attributes

resampled_ts <- ts(resampled_centered_resids_matrix,

start = start(centered_resids_stationary),

end = end(centered_resids_stationary),

frequency = frequency(centered_resids_stationary))

# Check dimensions: should be (n_dates-1) x n_sims

print(dim(resampled_ts))

# At time t = 0, diff_martingale process is equal is D_0 = S_0 (exp(-r * 0)*S_0)

# First cumsum the process to get exp(-r*t)*S_t

# Then multiply by exp(r*t) to have a process in risk neutral probability

# Step 1: Start with S0 at t=0

D0 <- S0 # since exp(-r*0) = 1

# Step 2: Cumsum to get discounted prices (e^{-rt} * S_t) under Q

# Add D0 as first row, then cumsum of innovations

discounted_paths <- D0 + apply(resampled_ts, 2, cumsum) # t=1..T

discounted_paths <- rbind(D0, discounted_paths)

discounted_paths <- ts(as.matrix(discounted_paths), start=start(sim_GBM),

frequency = frequency(sim_GBM))

time_points <- time(discounted_paths)

risk_neutral_prices <- ts(discounted_paths * exp(r * time_points),

start=start(sim_GBM),

frequency = frequency(sim_GBM))

head(risk_neutral_prices(, 1:5))

esgplotbands(risk_neutral_prices)

# =============================================================================

# I. Basic diagnostics

# =============================================================================

# No negative prices (log-normal support check)

n_negative <- sum(risk_neutral_prices < 0, na.rm = TRUE)

cat("Negative prices:", n_negative, "n")

stopifnot(n_negative == 0)

# Terminal distribution summary

S_T <- as.numeric(risk_neutral_prices(nrow(risk_neutral_prices), ))

cat("n--- Terminal price S_T summary ---n")

print(summary(S_T))

cat("Std dev:", sd(S_T), "n")

cat("Skewness:", moments::skewness(S_T), "n")

cat("Excess kurtosis:", moments::kurtosis(S_T) - 3, "n")

# =============================================================================

# II. Martingale checks

# =============================================================================

# E(exp(-r*T) * S_T) should equal S_0

T_years <- h

discount_T <- exp(-r * T_years)

mc_price <- discount_T * mean(S_T)

cat("n--- Martingale check ---n")

cat("S_0 :", S0, "n")

cat("E(exp(-rT) * S_T) :", round(mc_price, 4), "n")

cat("Absolute error :", round(abs(mc_price - S0), 4), "n")

# Check at every time point: mean discounted path should stay ~S0

discounted_paths_check <- risk_neutral_prices * exp(-r * time(risk_neutral_prices))

mean_discounted <- rowMeans(discounted_paths_check)

cat("nMean discounted price (first 6 and last 6 time points):n")

print(round(head(mean_discounted), 4))

print(round(tail(mean_discounted), 4))

# t-test: is E(exp(-rT)*S_T) = S0?

ttest <- t.test(discount_T * S_T-S0, mu = 0)

cat("nt-test H0: E(exp(-rT)*S_T) = S0n")

print(ttest)

# =============================================================================

# III. Distributional tests on log-returns

# =============================================================================

log_returns <- diff(log(risk_neutral_prices))

# Normality of cross-sectional log-returns at terminal date

lr_T <- as.numeric(log_returns(nrow(log_returns), ))

cat("n--- Normality tests on terminal log-returns ---n")

print(shapiro.test(sample(lr_T, min(5000L, length(lr_T))))) # Shapiro-Wilk (max n=5000)

print(ks.test(lr_T, "pnorm", mean(lr_T), sd(lr_T))) # KS vs normal

# Mean log-return should be close to (r - 0.5*sigma^2) * dt

dt <- 1 / frequency(risk_neutral_prices)

mean_lr <- mean(lr_T)

theoretical <- (r - 0.5 * sigma^2) * dt

cat("nMean terminal log-return :", round(mean_lr, 6), "n")

cat("Theoretical (r-s²/2)*dt :", round(theoretical, 6), "n")

# Variance ratio: empirical vs GBM theoretical

# Under GBM: Var(log S_T) = sigma^2 * T

empirical_var <- var(log(S_T))

theoretical_var <- sigma^2 * T_years

cat("n--- Variance ratio check ---n")

cat("Var(log S_T) empirical :", round(empirical_var, 4), "n")

cat("Var(log S_T) GBM theory :", round(theoretical_var, 4), "n")

cat("Ratio :", round(empirical_var / theoretical_var, 4), "n")

# =============================================================================

# IV. Option pricing — European calls and puts

# =============================================================================

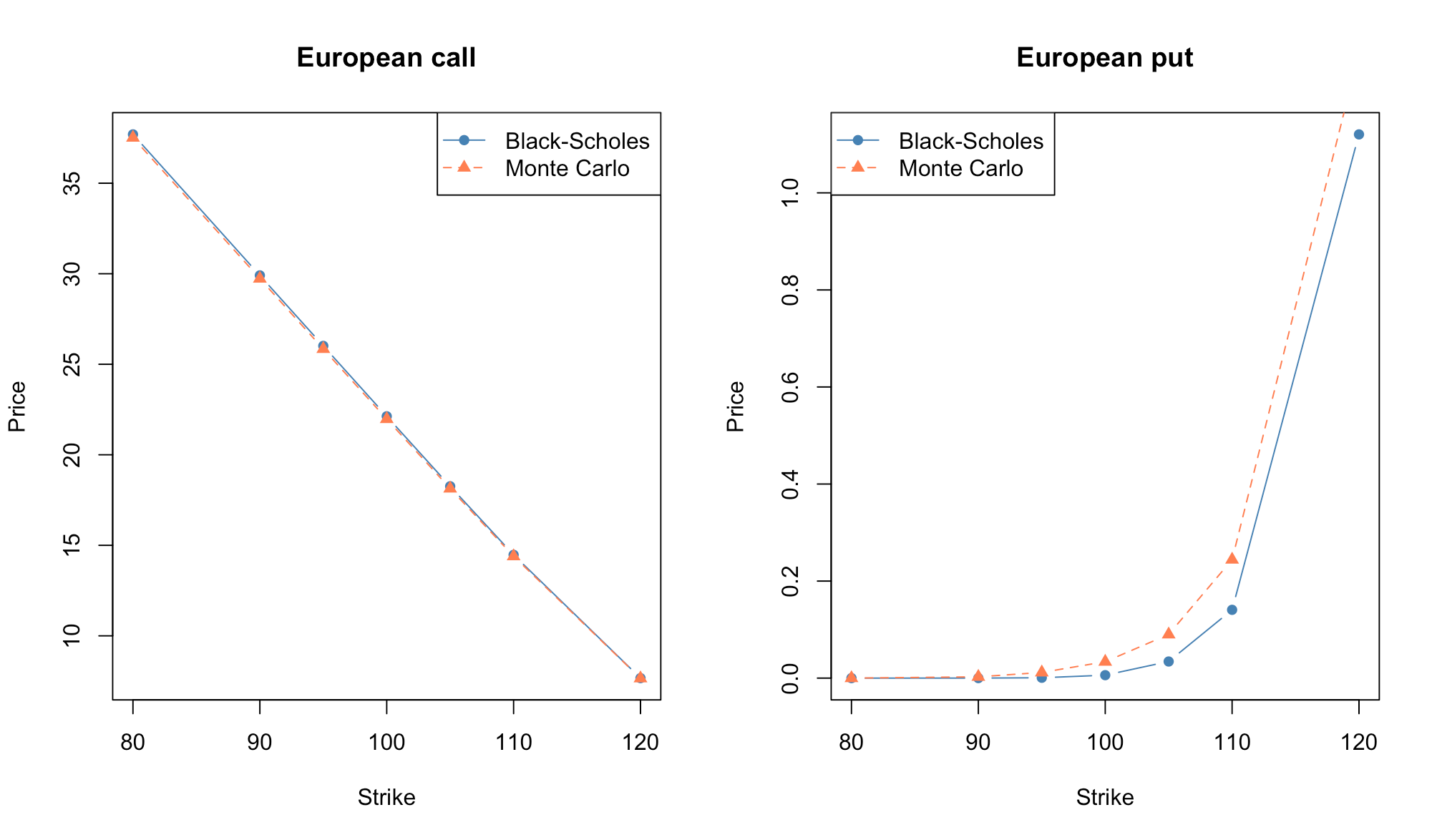

strikes <- c(80, 90, 95, 100, 105, 110, 120) # ITM to OTM

# -- Monte Carlo prices -------------------------------------------------------

mc_call <- sapply(strikes, function(K)

exp(-r * T_years) * mean(pmax(S_T - K, 0)))

mc_put <- sapply(strikes, function(K)

exp(-r * T_years) * mean(pmax(K - S_T, 0)))

# -- Black-Scholes prices -----------------------------------------------------

bs_call <- function(S, K, r, sigma, T) {

d1 <- (log(S/K) + (r + 0.5*sigma^2)*T) / (sigma*sqrt(T))

d2 <- d1 - sigma*sqrt(T)

S * pnorm(d1) - K * exp(-r*T) * pnorm(d2)

}

bs_put <- function(S, K, r, sigma, T) {

d1 <- (log(S/K) + (r + 0.5*sigma^2)*T) / (sigma*sqrt(T))

d2 <- d1 - sigma*sqrt(T)

K * exp(-r*T) * pnorm(-d2) - S * pnorm(-d1)

}

bsc <- sapply(strikes, function(K) bs_call(S0, K, r, sigma, T_years))

bsp <- sapply(strikes, function(K) bs_put(S0, K, r, sigma, T_years))

# -- Put-call parity check (MC) -----------------------------------------------

# C - P = S0 - K*exp(-rT) (forward parity)

pcp_mc <- mc_call - mc_put

pcp_th <- S0 - strikes * exp(-r * T_years)

pcp_err <- abs(pcp_mc - pcp_th)

# -- Summary table ------------------------------------------------------------

results <- data.frame(

K = strikes,

BS_call = round(bsc, 4),

MC_call = round(mc_call, 4),

err_call = round(abs(mc_call - bsc), 4),

BS_put = round(bsp, 4),

MC_put = round(mc_put, 4),

err_put = round(abs(mc_put - bsp), 4),

PCP_error = round(pcp_err, 4)

)

cat("n--- European option prices: MC vs Black-Scholes ---n")

print(results, row.names = FALSE)

# -- Plot ---------------------------------------------------------------------

par(mfrow = c(1, 2))

plot(strikes, bsc, type = "b", pch = 16, col = "steelblue",

xlab = "Strike", ylab = "Price", main = "European call")

lines(strikes, mc_call, type = "b", pch = 17, col = "coral", lty = 2)

legend("topright", legend = c("Black-Scholes", "Monte Carlo"),

col = c("steelblue", "coral"), pch = c(16, 17), lty = c(1, 2))

plot(strikes, bsp, type = "b", pch = 16, col = "steelblue",

xlab = "Strike", ylab = "Price", main = "European put")

lines(strikes, mc_put, type = "b", pch = 17, col = "coral", lty = 2)

legend("topleft", legend = c("Black-Scholes", "Monte Carlo"),

col = c("steelblue", "coral"), pch = c(16, 17), lty = c(1, 2))

par(mfrow = c(1, 1))