(Acest articol a fost publicat pentru prima dată pe DataGeeekși cu amabilitate a contribuit la R-bloggeri). (Puteți raporta problema legată de conținutul acestei pagini aici)

Doriți să vă distribuiți conținutul pe R-bloggeri? dați clic aici dacă aveți un blog, sau aici dacă nu aveți.

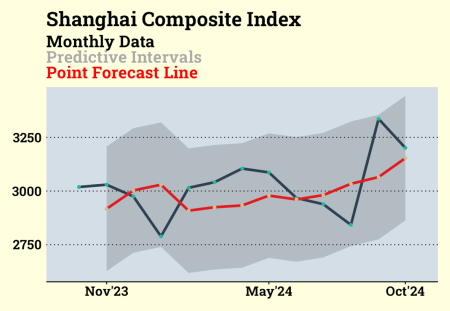

Shanghai Composite nu pare să fie într-un punct ideal pentru intrare.

Cod sursă:

library(tidyverse)

library(tidyquant)

library(timetk)

library(tidymodels)

library(modeltime)

library(workflowsets)

#Shanghai Composite Index (000001.SS)

df_shanghai <-

tq_get("000001.SS", from = "2015-09-01") %>%

tq_transmute(select = close,

mutate_fun = to.monthly,

col_rename = "sse") %>%

mutate(date = as.Date(date))

#Splitting

split <-

df_shanghai %>%

time_series_split(assess = "1 year",

cumulative = TRUE)

df_train <- training(split)

df_test <- testing(split)

#Time series cross validation for tuning

df_folds <- time_series_cv(df_train,

initial = 77,

assess = 12)

#Preprocessing

rec <-

recipe(sse ~ date, data = df_train) %>%

step_mutate(date_num = as.numeric(date)) %>%

step_date(date, features = "month") %>%

step_dummy(date_month, one_hot = TRUE) %>%

step_normalize(all_numeric_predictors())

rec %>%

prep() %>%

bake(new_data = NULL) %>% view()

#Model

mod <-

arima_boost(

min_n = tune(),

learn_rate = tune(),

trees = tune()

) %>%

set_engine(engine = "auto_arima_xgboost")

#Workflow set

wflow_mod <-

workflow_set(

preproc = list(rec = rec),

models = list(mod = mod)

)

#Tuning and evaluating the model on all the samples

grid_ctrl <-

control_grid(

save_pred = TRUE,

parallel_over = "everything",

save_workflow = TRUE

)

grid_results <-

wflow_mod %>%

workflow_map(

seed = 98765,

resamples = df_folds,

grid = 10,

control = grid_ctrl

)

#Accuracy of the grid results

grid_results %>%

rank_results(select_best = TRUE,

rank_metric = "rmse") %>%

select(Models = wflow_id, .metric, mean)

#Finalizing the model with the best parameters

best_param <-

grid_results %>%

extract_workflow_set_result("rec_mod") %>%

select_best(metric = "rmse")

wflw_fit <-

grid_results %>%

extract_workflow("rec_mod") %>%

finalize_workflow(best_param) %>%

fit(df_train)

#Calibrate the model to the testing set

calibration_boost <-

wflw_fit %>%

modeltime_calibrate(new_data = df_test)

#Accuracy of the finalized model

calibration_boost %>%

modeltime_accuracy(metric_set = metric_set(mape, smape))

#Predictive intervals

calibration_boost %>%

modeltime_forecast(actual_data = df_merged %>%

filter(date >= last(date) - months(12)),

new_data = df_test) %>%

plot_modeltime_forecast(.interactive = FALSE,

.legend_show = FALSE,

.line_size = 1.5,

.color_lab = "",

.title = "Shanghai Composite Index") +

geom_point(aes(color = .key)) +

labs(subtitle = "Monthly Data

Predictive Intervals

Point Forecast Line") +

scale_x_date(breaks = c(make_date(2023,11,1),

make_date(2024,5,1),

make_date(2024,10,1)),

labels = scales::label_date(format = "%b'%y"),

expand = expansion(mult = c(.1, .1))) +

ggthemes::theme_wsj(

base_family = "Roboto Slab",

title_family = "Roboto Slab",

color = "blue",

base_size = 12) +

theme(legend.position = "none",

plot.background = element_rect(fill = "lightyellow", color = "lightyellow"),

plot.title = element_text(size = 24),

axis.text = element_text(size = 16),

plot.subtitle = ggtext::element_markdown(size = 20, face = "bold"))